To build a better New York City, we must grapple honestly with the past.

Bronx, Neighborhood D4: "There is a steady infiltration of negro, Spanish and Puerto Rican into the area."

Brooklyn, Neighborhood C6: "Formerly a fine residential section of brick and stone singles but area is being adversely affected by infiltration of lower grade people from the north."

Manhattan, Neighborhood D1: "In earlier years the whole lower East Side was a dumping ground for the hordes of immigrants entering the U.S. thru N.Y.C."

Queens, Neighborhood D34: "Negro colony."

Staten Island, Neighborhood D8: "This area may very conceivably develop into a colored concentration."

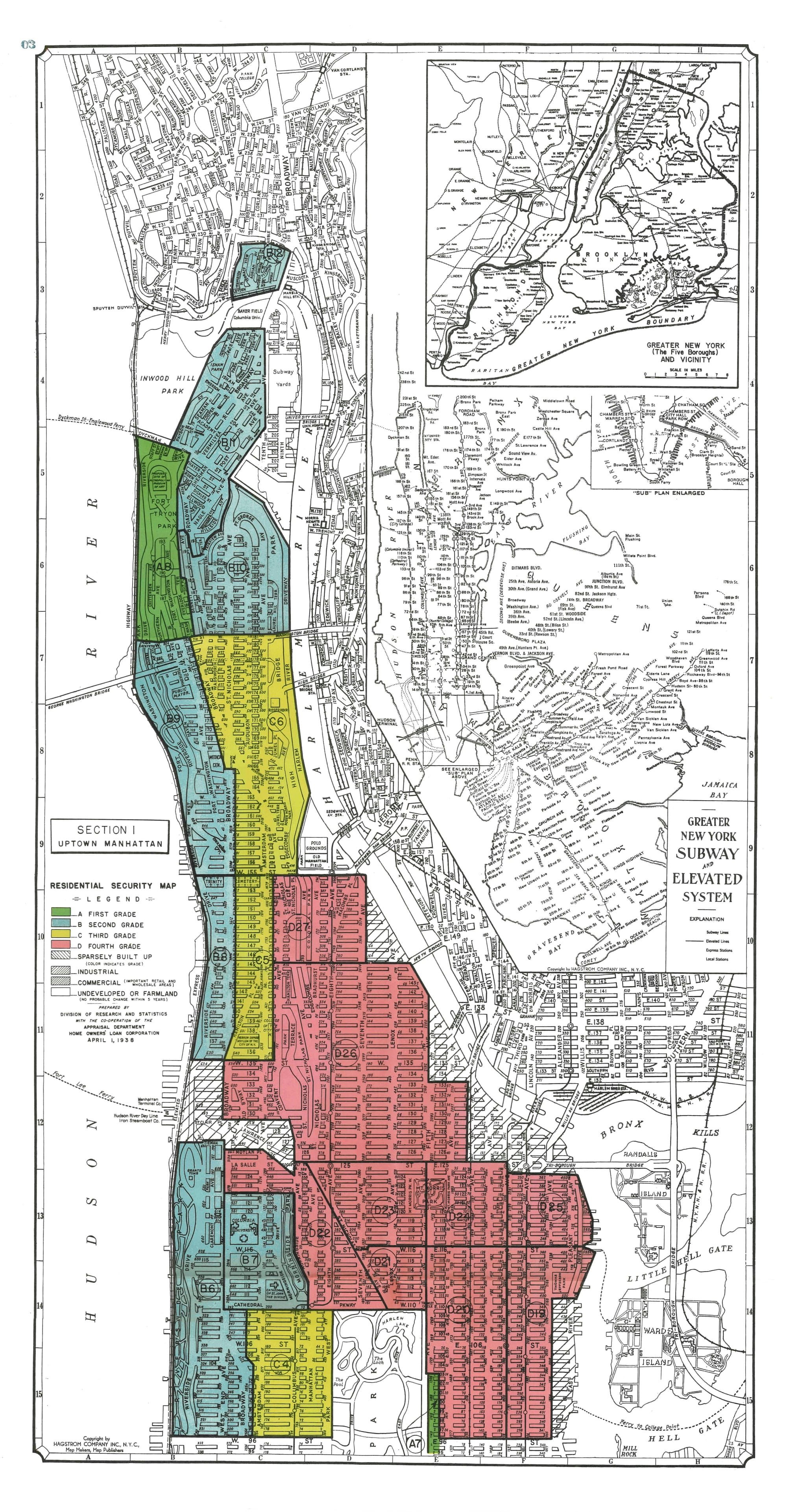

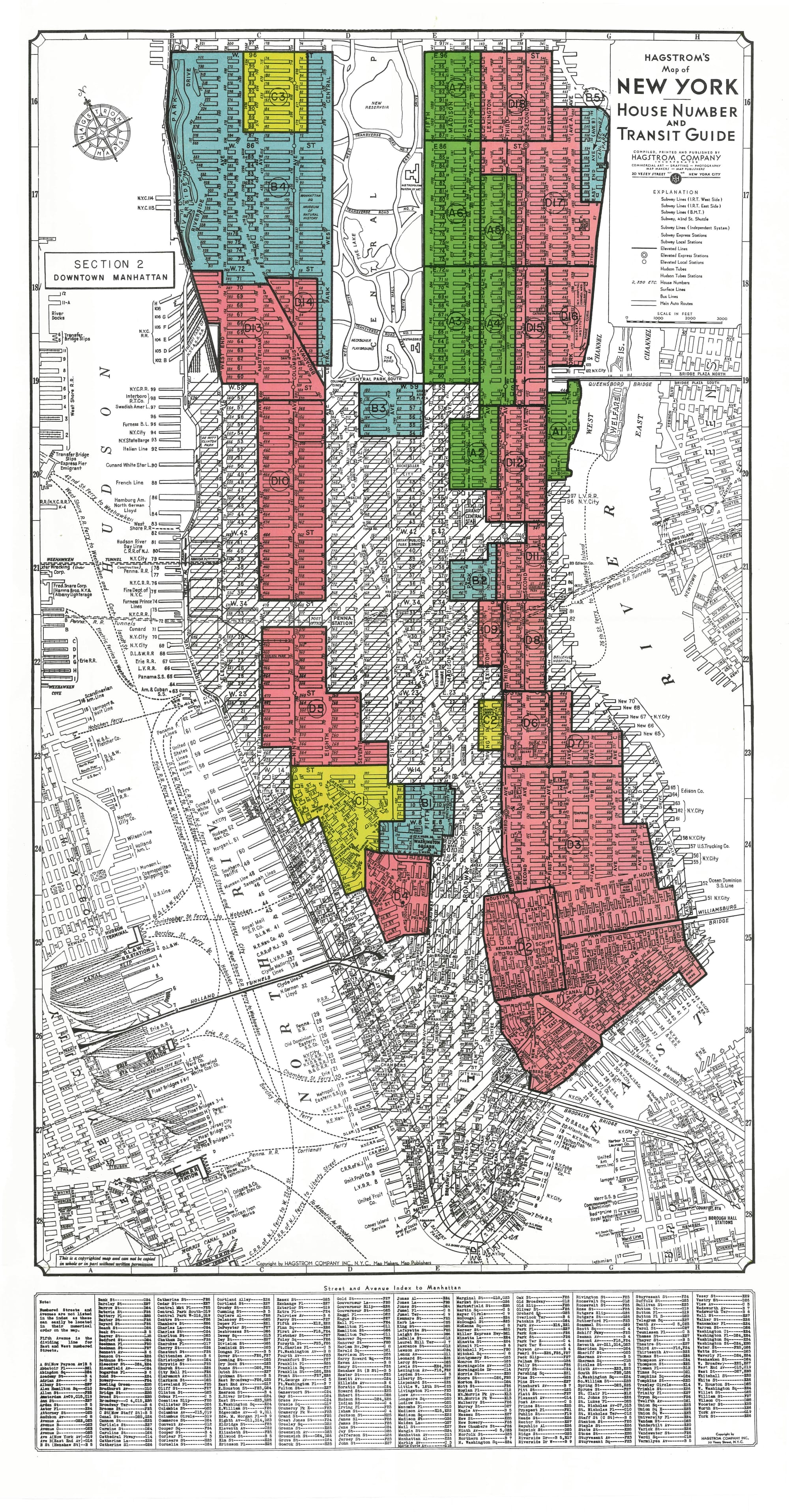

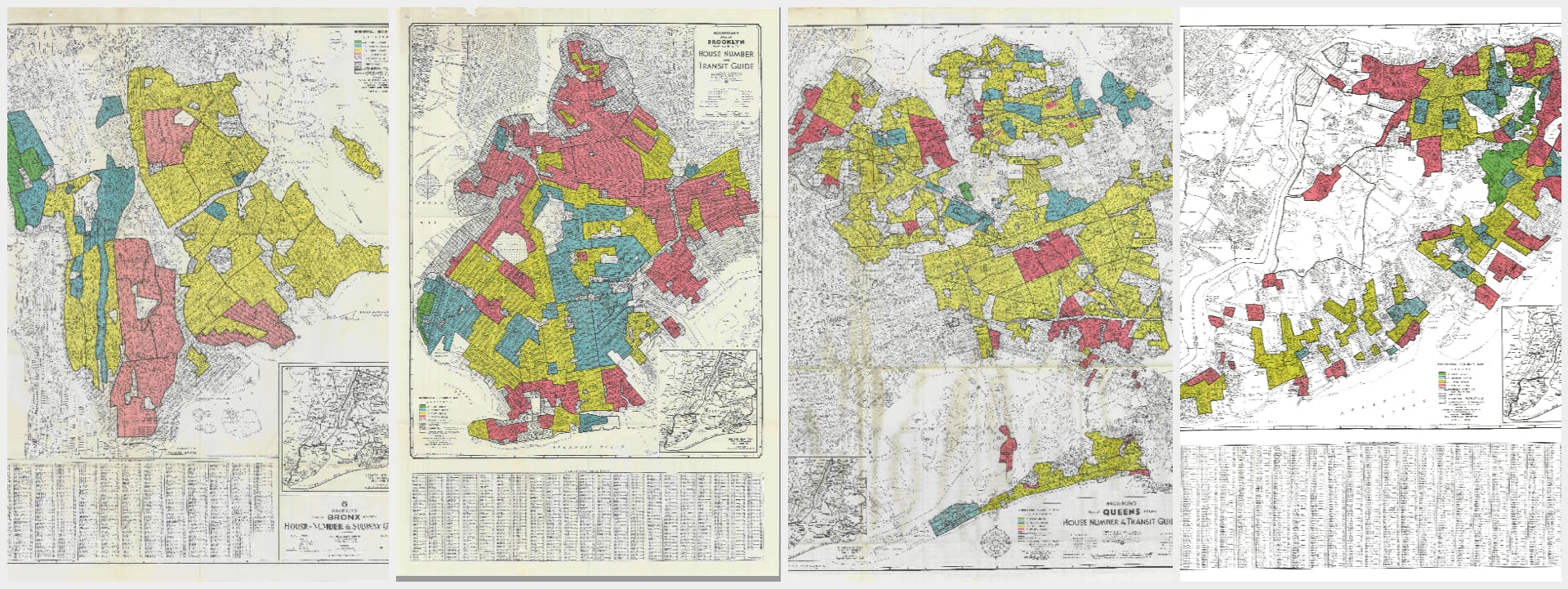

These racist and xenophobic excerpts are from the now-infamous redlining maps of New York City drawn by Home Owners Loan Corporation (HOLC) appraisers in the late 1930s. HOLC, a government-sponsored corporation, was created by Congress in 1933 to rescue a housing market in free fall during the Great Depression by providing long-term, stable-payment and amortizing mortgages to distressed borrowers at risk of foreclosure. In doing so, HOLC and subsequent New Deal housing programs (such as the Federal Housing Administration, or FHA), as well as the Veterans Administration (through the 1944 GI Bill), made owning a home far less expensive than renting in much of the country, thereby creating the American homeownership society we know today and providing a powerful tool for intergenerational wealth accumulation.

Unfortunately, as the quotes above document, these policies were segregationist by design, penalizing people and communities of color across the United States and encouraging white families to flee cities for segregated, suburban neighborhoods. HOLC created a system of grades to guide banks as they determined whether to extend loans to prospective borrowers. The grades were color-coded: A ("Best" and colored green), B ("Still Desirable," blue), C ("Declining," yellow), and D ("Hazardous," red). The appraisers who were employed by HOLC to create these maps based the grades on housing characteristics, economic and environmental conditions, transit access and — arguably more than anything else — the racial and ethnic makeup of a neighborhood's residents.

Consider the following excerpts from HOLC maps drawn for Westchester County in New York, as well as Essex County, Union County and Bergen County in New Jersey. These highly rated neighborhoods were specifically commended for residents' "character" as well as the use of zoning restrictions, deeds and property destruction as tools for segregating African Americans and Italians (who were presumed to have lower character):

Westchester County, Neighborhood A1: "Favorable Influences: Character of occupant and improvements, zoning restrictions and attractiveness of location."

Essex County, Neighborhood A25: "Wildwood from North Fullerton to Grove contains older houses and Wildwood from Grove east contains Italians. This latter settlement is small and cannot spread as it is hemmed in all sides by new and better developments."

Union County, Neighborhood B36: "Negro families are concentrated around Maple, W. Milton, and Elm Avenue in houses which have been declared unfit for habitation and condemned. This element will therefore move out of the area."

Federally supported redlining drove white flight by conflating proximity to Black people with declining home values.

These New Deal programs certainly did not invent racist exclusion or valuation in real estate, but they did institutionalize, codify and invest tremendous federal resources in the idea that Blacks, certain immigrants and other populations lacking "character" or "pride" were not just unworthy of homeownership but were "detrimental influences" destined to drive down property values. Because of the tremendous power of the federal government, this became the logic of investment (and disinvestment) that drove development in New York City and its surrounding suburbs throughout most of the 20th century.

Federally supported redlining drove white flight by conflating proximity to Black people with declining home values. Between 1940 and 1980, the population of New York City fell by almost 400,000 people, while the population of the metropolitan area grew by more than 4 million. Redlining also laid the groundwork for urban renewal, which James Baldwin famously called "Negro removal."

A growing body of research blames last century's housing policies for setting neighborhoods on drastically different and decades-long trajectories.

We can see the foreshadowing of this practice in the Union County HOLC appraiser's language above. This program was ostensibly designed to "renew" central city neighborhoods in desperate need of investment, but it largely served as a land grab by real estate developers. Of the projects for which we have records, more than 29,000 families were displaced by urban renewal projects in New York City, 41% of whom were people of color. And thanks to poor record-keeping at the time, we can assume these numbers represent only a minority of projects.

This history continues to define current-day New York in more ways than many care to admit. Although the city has experienced tremendous change since the New Deal era, a growing body of research blames last century's housing policies for setting neighborhoods on drastically different and decades-long trajectories, with growth and wealth accumulation on the one hand and decline and poverty on the other.

Redlined areas are more segregated and have lower rates of economic mobility than neighboring communities. These areas were also more vulnerable to often-predatory subprime mortgage lending during the housing boom of the early 21st century and are predicted to be hit hardest by climate change in future decades. Crucially, these policies also seem to have increased and concentrated crime and incarceration.

At their core, New Deal programs intended to create opportunities for neighborhood stability and wealth accumulation, but they segregated it.

This historical background also provides an important lens through which to understand what makes neighborhoods and cities thrive. Redlining and its inverse (i.e., "greenlining" of white, suburban neighborhoods) offer models. At their core, New Deal programs intended to create opportunities for neighborhood stability and wealth accumulation, but they segregated it and — generally — moved it out of cities. The intentional decision to categorize the presence of Blacks and poor families as "detrimental influences" was driven by a belief in the importance of community, though this belief was tragically corrupted by racism, classism and xenophobia.

So when we search for solutions to the problems of today's New York City, such as a growing crisis of housing affordability, rapidly accelerating climate change, and widening economic inequality and instability — and their manifestations as homelessness, crime, poverty and polarization — we do not need to jump first and most enthusiastically to policing. Research has repeatedly shown that investing in families and communities — especially in racially and economically isolated communities — can substantially improve the lives of people who live there and benefit the broader economy.

Unsurprisingly, housing is key. Providing supportive housing and investing in affordable housing are proven solutions to homelessness, eviction and economic instability. Relatedly, access to mortgage credit can reduce crime. Community-based nonprofit organizations, as well as more informal neighborhood groups and social ties, are also tremendously important for building resiliency to a wide range of concerns, from crime to vulnerability to the worsening threats of climate change. These investment-focused alternatives to our current approach of criminalizing and institutionalizing poverty are not only more likely to have sustainable, long-term and positive impacts but are especially important in light of the myriad costs policing imposes on families and communities.

It has become somewhat trite to say we are at a crucial point in history, but it is difficult to overemphasize the precarious situation New York City — as well as the United States more broadly — faces. The COVID-19 pandemic has already killed well over 1 million Americans and (as of this writing) continues to kill more people each week (approximately 4,000) than the number of people killed in the attacks of Sept. 11, 2001. More than 44,000 of these deaths have occurred in New York City. The economic fortunes of hundreds of millions of Americans have been harmed through an unprecedented unemployment catastrophe caused by the pandemic, which some are calling a "mass-disabling event." What's more, the expansion of remote work is threatening the commercial viability of many urban centers, and even those living in subsidized housing are finding it challenging to keep up with rent.

This unprecedented crisis has come only a decade after another unprecedented crisis, the one caused by the collapse of the world financial market, the center of which was in New York City. Just as the Great Depression called for action, now is the time to pour resources into those communities that have borne and will continue to bear the brunt of these multiple, self-reinforcing catastrophes.